Quote of the Week

“In every difficult situation is potential value. Believe this, then begin looking for it.” – Norman Vincent Peale

Tech Corner

Last week was another week of “where’s the beef?” returns, with most indexes up around 1%. The outlier was the Nasdaq up +2.06%. What I find interesting is the year-to-date performance of the Nasdaq. Starting out 2021, the Nasdaq was the darling of Wall Street through January and February. However, the trend changed quickly with the “high flying stay at home” tech companies rapidly falling behind the more staid names. Year to date, the Nasdaq is only up +6.68%, while the S&P 500 is up +11.93%, and the stodgy Dow is up +12.82%.

We are still in a deep Quad II which is good for equities and commodities. We are positioned accordingly.

Last month the “Jobs Report” came in at a disappointing +250,000 while a million new jobs were expected. However, that is all going to change over the next three or so months. Today roughly 15 months after Covid began, there are still 16 million workers collecting unemployment insurance. For reference, at the peak of the Great Financial Crisis, in May of 2009, there were 6.5 million workers collecting unemployment insurance. So, we are still at 2.5 times the peak of the GFC in terms of the number of insured unemployment. Meanwhile, in May of 2009, according to JOLTS data (Job Openings, Total Nonfarm), there were just 2.5 million job openings. Today there are 8.1 million job openings.

To be clear, job openings fell precipitously from 7.1 million in January 2020 to a low of 4.6 million in April 2020. However, they have risen almost every month since then and now stand at one million job openings higher than in January 2020. Yet, the number of initial jobless claimants remains at 16 million or roughly ten times the 1.7 million job unemployment claimants in January 2020.

There are several reasons why such a stark disconnect exists today. One reason is that many would-be workers are afraid to return to the workforce due to Covid. Another reason is that many would-be workers have children who are not in school, and childcare options are expensive or unavailable. Another reason is that many would-be workers earn enough from enhanced unemployment benefits. Therefore, they do not have the economic incentive to return to work if working offers them only a few dollars more per hour than they are receiving from unemployment.

That is about to change soon. First, there is a red state, blue state fault line emerging in recent months, creating a genuine labor market rift. Many “red” states (21 as of the latest count) have recently announced that they will cease accepting Federal supplement unemployment aid effective between June and mid-July. These 21 states, some of them large like Texas and Ohio, account for over 112 million people or roughly 35% of the US workforce. By the way, Arizona is one of those states. This will end the $300/week supplemental payment that currently adds 50% or more to the underlying state benefit.

Further, these states will stop the extended benefits option, and finally, these states will also stop accepting PUA benefits that go to “independent or GIG” workers. All told, this will effectively end unemployment benefits eligibility for roughly two-thirds of unemployment beneficiaries in these states, or approximately 3.7 million people. Also, add in the fact that “rent abatement” programs will soon stop, so people will have to start paying rent again.

What will happen as a result? First, obviously, continuing jobless claims will fall precipitously over the next eight weeks. Second, there is a very high probability that the jobs numbers will be solid for the months of June, July, and August as these beneficiaries find their way back into the workforce in increasing numbers. Finally, add in the fact that the Federal Supplemental benefits expire nationally in September we should see strong job growth into the fall.

But wait, there’s more. One reason people are not retuning to the labor force is a lack of childcare due to remote or hybrid schooling. As of March, only half of the schools across the US were fully reopened. So one of the most significant changes to the labor force will likely come in September when most schools across the nation fully reopen to full-time in-person learning.

In conclusion, we expect the job market to change massively in the following months for the better.

Larry’s Thoughts

Last week we received a lot of responses to the housing price increases. I hope you find this article from “The Real Economy Blog” on the “nuts and bolts” for the amazing increases in housing prices useful.

North American housing markets remain bullish

MAY. 27, 2021, BY TROY MERKEL AND NICK GRANDY

In spite of the pandemic, the US and Canadian housing markets have seen significant growth over the past year as individuals and families stuck in apartments were driven to the suburbs in search of bigger homes with space to live, work and play. In addition to a rise in demand for single-family housing, housing supply shortages, higher material prices, fewer available lots and ongoing zoning restrictions are driving existing and new home prices up across both countries.

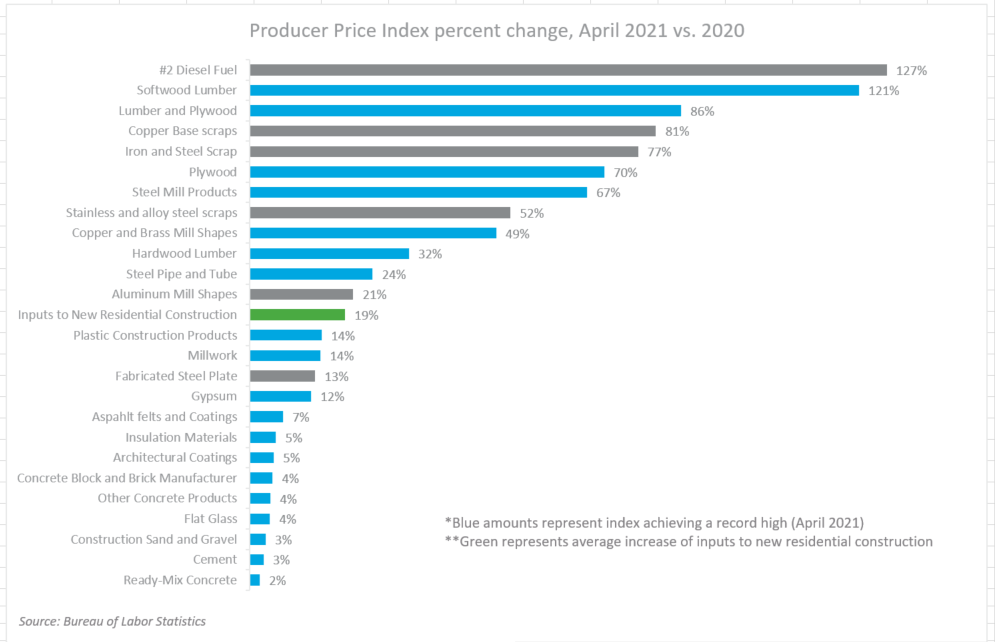

Construction material prices have been on the rise since the middle of 2020, bringing with them higher retail home prices. According to the National Association of Home Builders, the surge in lumber prices alone has resulted in the average price of a new single-family home in the United States rising by $36,000, to about $330,000, with lumber representing about 11% of the total value. Lumber is not the only material tracking record highs. The US Producer Price Index hit new highs in April for a significant number of building materials, including steel pipe and tubes, and plastic products, further driving up construction costs.

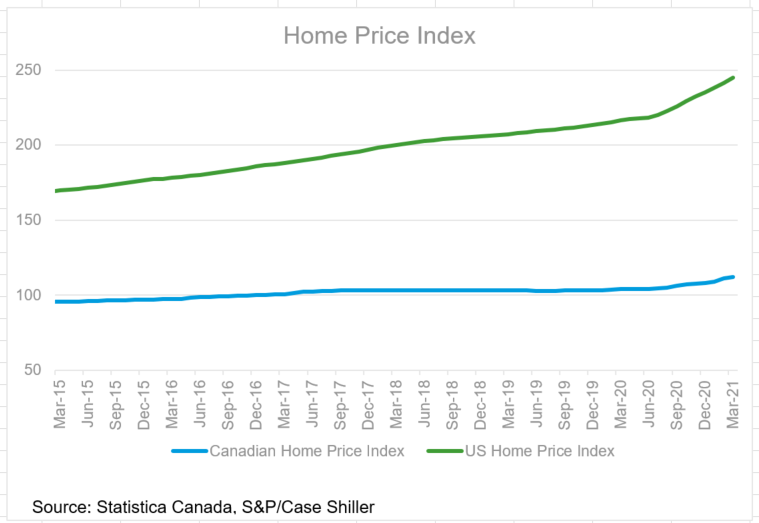

In addition to the cost of materials, contractors have found difficulty securing permitted lots to build on. Municipalities in both Canada and the United States have created obstacles to development in the suburban markets that are now attracting new homebuyers looking for indoor and outdoor space at home. Laws that limit building often require minimum lot sizes, parking requirements and prohibitions on multi-family housing, which drive up costs and keep families stuck in their communities. In Canada, challenging suburban building restrictions such as these and a lack of available lots are driving more developers to continue building multi-family housing instead of single-detached and semi-detached units that Canadian consumers demand. This disconnect between market supply and demand will continue to send Canadian home prices soaring beyond the 11.9% year-over-year increase already seen in the major markets.

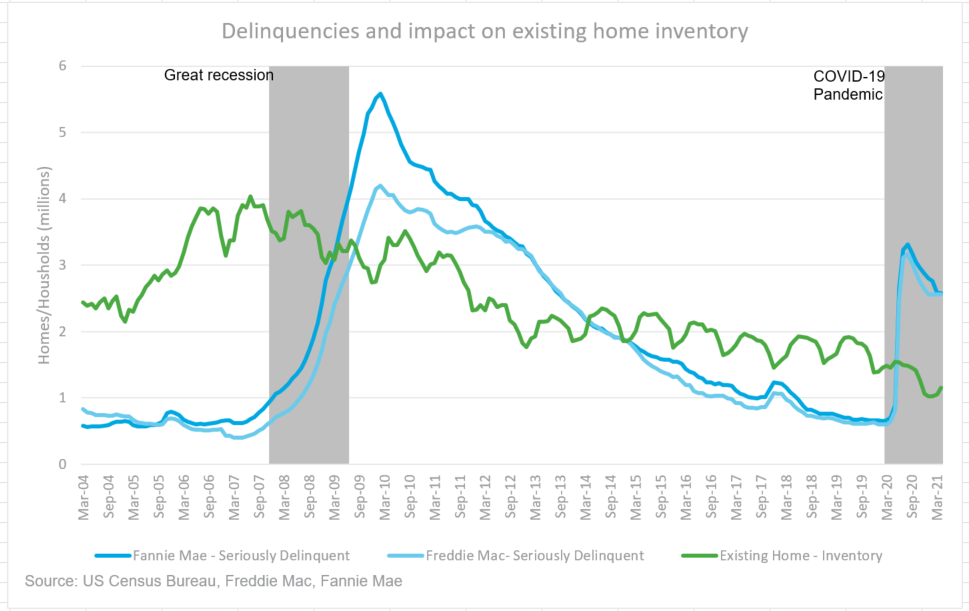

To help combat the impact of the pandemic on households, governments of both countries have enforced foreclosure moratoriums, allowing for forbearance on mortgages to help prevent a housing crisis. (The US moratorium is set to end on June 30, 2021. Data from the Canadian Bankers Association shows that approximately 97.5% of households that deferred or skipped mortgages have resumed payment as of February 2021.) These measures prevented significant foreclosures by helping keep households afloat amid an inconsistent pandemic impact across the economy. At the same time, they have also led to a decline in inventory, and, amid increased housing demand, have contributed to the rise in prices of existing homes. Research from the US Federal Reserve attributes 0.6% of the price increase of existing homes across the United States to foreclosure protections.

Despite the headwinds facing the housing ecosystem, the industry has continued to lead the economic recovery in North America. For this trend to continue its bullish path, some important policy shifts need to occur. The US and Canadian governments should look to reduce tariffs—in particular those on Canadian lumber—to reduce the costs of supply and allow for continued housing affordability.

In addition, federal and local municipalities should develop policies to promote strategic residential development that supports growth and supplies new housing in their communities. President Biden’s infrastructure plan, which calls for building and retrofitting 2 million homes to help address affordability, will help loosen supply-side restraints. The administration has also requested that Congress eliminate or reduce exclusionary zoning laws at a state and local level.

Prime Minister Justin Trudeau recently announced the tightening of lending restrictions in an attempt to slow demand in the Canadian housing market. While policies such as this can be enacted quickly to help slow what many see as a runaway housing market, it is critical that the more arduous road of supply-side solutions, such as zoning reform, supply chain management and other builder-friendly policies, be on Canada’s longer-term agenda.

“North American housing markets remain bullish.” Real Economy 27 May 2021, https://realeconomy.rsmus.com/north-american-housing-markets-remain-bullish/