Quote of the Week

“The best time to plant a tree was 20 years ago. The second best time is right now.” – Old Chinese Proverb

Tech Corner

April ended just as three out of the last four months with a substantial down day. That’s Murphy’s Law. April was a pretty good month for the markets and the portfolios we manage. Year to date the Dow is up +10.68%, the S&P 500 is up +11.32%, the Nasdaq is up + 8.34% and the MSCI-EAFE is up +6.72%. Starting in Mid March and through most of April, there has been a swing from growth outperformance to value outperformance. That is why the Dow and the S&P 500 have come back to lead the Nasdaq year-to-date. It looks like the trend is switching back to growth which is where we are mostly positioned.

We are still firmly in Quad II which is good for stocks and commodities. We don’t see any changes coming soon on the horizon, so it looks like some clear sailing for the foreseeable future.

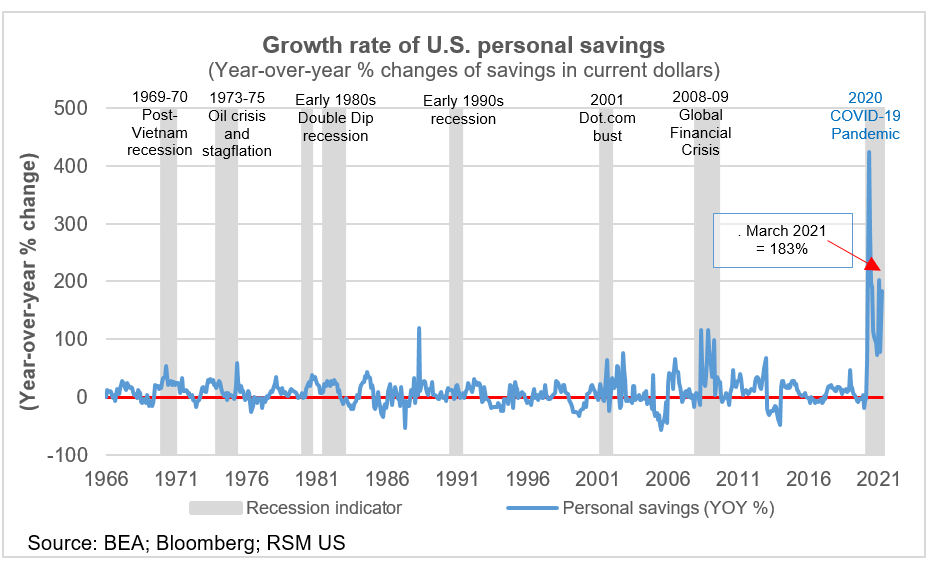

US GDP surged at an annualized rate of 6.4% in the first quarter. Two rounds of government stimulus helped the economy rise within 0.9% of its all time high. The economy has recovered to just slightly below where it was before Covid-19 hit us last year. I am especially encouraged with the huge amount of personal savings (see Larry’s Thoughts), as the last figure I saw was $1.9 trillion. This is a huge jump in savings and a lot of that money will be spent.

S&P earnings are on track according to estimates to grow 45.8% for the first quarter. Our tracking has earnings growing at 61%, but there are still a lot of companies still to report.

The big news this week will be the April employment report. The report will provide evidence of whether the stimulus and re-openings are going to pull people back to work. The problem is that many workers are making just as much or in some cases more by staying home drawing benefits. What I hear is that employers are having trouble filling their job openings.

We are still allocated to stocks and commodities and staying away from the bond market.

Larry’s Thoughts

Personal income rises 21.1% in March, with savings up 27.6%

APR. 30, 2021 BY JOSEPH BRUSUELAS

The impact of the $1.9 trillion in fiscal aid put on the table this year bolstered U.S. personal income by a record 21.1% in March, resulting in a 4.2% increase in personal spending.

Income excluding government transfers increased by 0.9% on the month. Compensation increased by 1%, while wages and salaries advanced by 1.1%. Those direct cash transfers resulted in a 23.6% increase in disposable income.

On a three-month average annualized pace, those gains resulted in a jump of 14.6% in spending, which is well above the 10.7% gain in spending in the first-quarter gross domestic product report published on Thursday. We now expect the first estimate of first-quarter GDP to be revised upward from 6.4% to closer to 7% before all is said and done.

In addition, the substantial increase in savings strongly suggests that there is risk of a much quicker pace of GDP growth in the current quarter relative to our forecast of 10.7%.

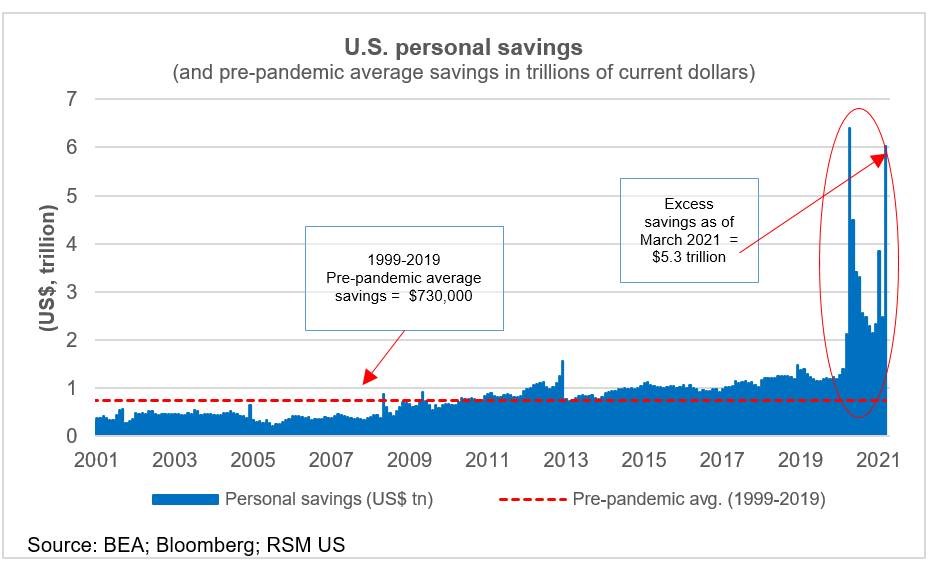

Direct-income transfers not only boosted spending but they also resulted in an increase in the U.S. savings rate to 27.6% in March from 13.9% in February. In dollar terms, U.S. household savings stand at $6.0 trillion, which is well above the pre-pandemic 20-year average of $730 billion.

The data implies that American households are now in a position to repair balance sheets by paying down debt while creating sizeable cash buffers against future instability. This will almost certainly support a period of household spending over the next three months that will be one for the record books.

Inside the report, the core personal consumption deflator on a year-ago basis increased from 1.4% in February to 1.8% in March. This is the Federal Reserve’s primary policy variable and is in line with the central bank’s forecast of higher inflation.

Yet even with the base effects of the collapse in demand and prices a year ago, it is still below the Fed’s 2% target.

In our estimation, the increase in this metric — the single best predictor of long-term inflation — will do little to alter the path of policy out of the central bank because of perceived risk to the economic outlook around inflation.

For more information on how the coronavirus pandemic is affecting midsize businesses, please visit the RSM Coronavirus Resource Center.

Brusuelas, Joseph “Personal income rises 21.1% in March, with savings up 27.6%.” The Real Economy Blog, https://realeconomy.rsmus.com/personal-income-rises-21-1-in-march-with-savings-up-27-6/ Accessed 4 May 2021